NHS Pension Annual Allowance: How It’s Calculated, With an Example

The Annual Allowance (AA) is one of the most misunderstood parts of the NHS Pension Scheme, and one of the main reasons doctors and consultants face unexpected tax bills.

You may assume it relates to how much you contribute, but it doesn’t.

It’s based on how much your pension grows each year.

This guide explains how it works, why it catches people out, and what you can do about it.

What Is the Annual Allowance?

The Annual Allowance is a limit on how much your pension can increase in value in a tax year before a tax charge may apply.

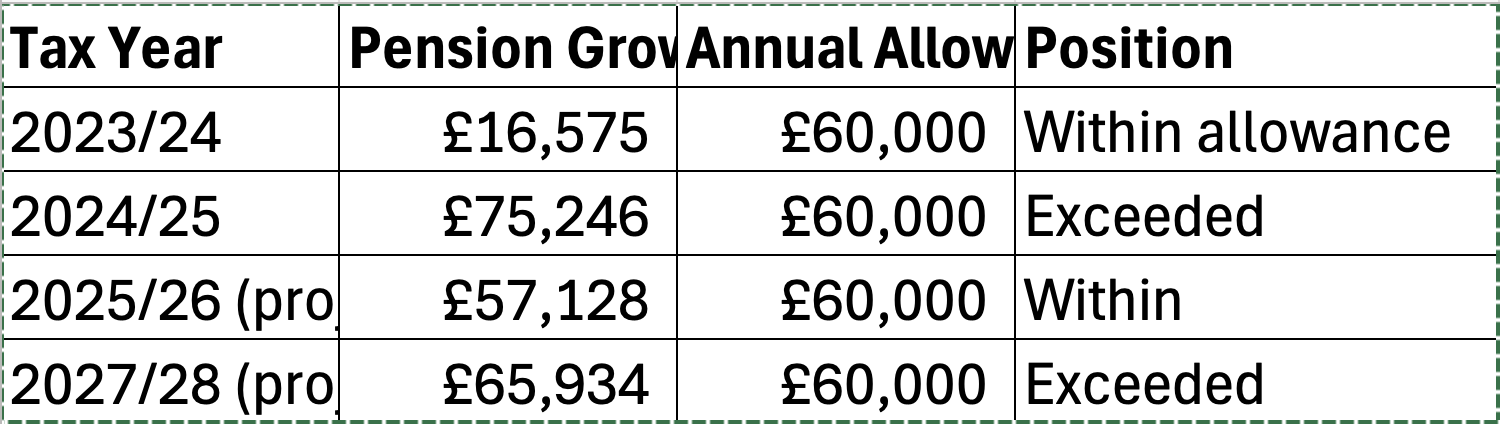

Current limit: £60,000 per year

Based on growth, not contributions

Different to conventional workplace pension which is based on contributions

This is why NHS pensions behave very differently from private pensions.

How NHS Pension Growth Is Calculated

Your pension growth (called the Pension Input Amount) is calculated by:

Looking at your pension value at the start of the year

Looking at your pension value at the end of the year

Adjusting for inflation

Measuring the increase

That increase is then tested against the £60,000 Annual Allowance.

Why this causes problems

Your pension growth can increase due to:

pay rises

promotions

extra sessions (PAs)

inflation adjustments

Even if your take-home pay hasn’t changed much

Real Example (Consultant Case)

Here’s a simplified example based on a real consultant scenario:

In 2024/25, pension growth exceeded the allowance by over £15,000

This creates a tax charge, even though no extra cash was received.

What Happens If You Exceed the Annual Allowance?

If your pension growth exceeds the allowance:

the excess is added to your taxable income

you pay income tax on it

this can result in large, unexpected tax bills

Especially for senior consultants

Carry Forward (important)

You can use unused allowance from the previous 3 tax years.

This can reduce or eliminate a tax charge—but:

it’s not automatic

it must be calculated carefully

many people don’t realise they’ve already used it

How to Reduce NHS Pension Tax Charges

There’s no one-size-fits-all solution, but common strategies include:

1. Adjusting Work Patterns

Reducing sessions (PAs) can reduce pension growth.

Dropping one PA could reduce pension growth to near zero in a future year

But, it will reduce long-term pension income

2. Using Scheme Pays

Instead of paying the tax yourself:

your NHS Pension Scheme pays it for you

your future pension is reduced

You pay interest on the outstanding amount

This spreads the cost over time

3. Planning Retirement Timing

When you take your pension affects:

growth

tax exposure

total benefits

Small timing changes can have large financial impacts.

4. Scenario Analysis

The most effective approach is:

modelling different scenarios before you make decisions

This allows you to:

see future tax exposure

compare options

avoid surprises

Why This Matters

The NHS pension is extremely valuable but:

tax can reduce that value significantly

decisions are often made without full visibility

small changes can create large outcomes

Most clinicians only realise this after receiving a tax bill

Final Thought

The Annual Allowance isn’t just a tax rule, it’s a key part of your overall pension strategy.

Understanding it properly can mean:

avoiding unnecessary tax

making better career decisions

protecting your long-term retirement income

Get Your NHS Pension Calculation

At Your NHS Pension, we provide:

clear pension projections

Annual Allowance calculations

scenario modelling

So you can understand:

your current position

your future tax exposure

your best options